Six Years of Synctera: Built to Win

March 30, 2026

A company is never in a “completed” state, but many of the ones that are succeeding are the ones who stick as close to their original vision as possible without changing their core thesis and principles.

Even before we founded Synctera (six years ago today!), we had a clear idea of who we wanted to be at our core: a solution to the deep complexity of building a FinTech in banking and embedded finance.

Originally, when we first talked about it, the genesis of Synctera was to deeply focus on compliance and risk in FinTech and create a solution that could be added to other platforms. Cool idea, just not a crazy enough challenge and probably not a big enough TAM to sustain venture-style growth. We pivoted and expanded on that idea to be the full solution: everything you need to build, run, and operate a FinTech. Basically, banking in a box.

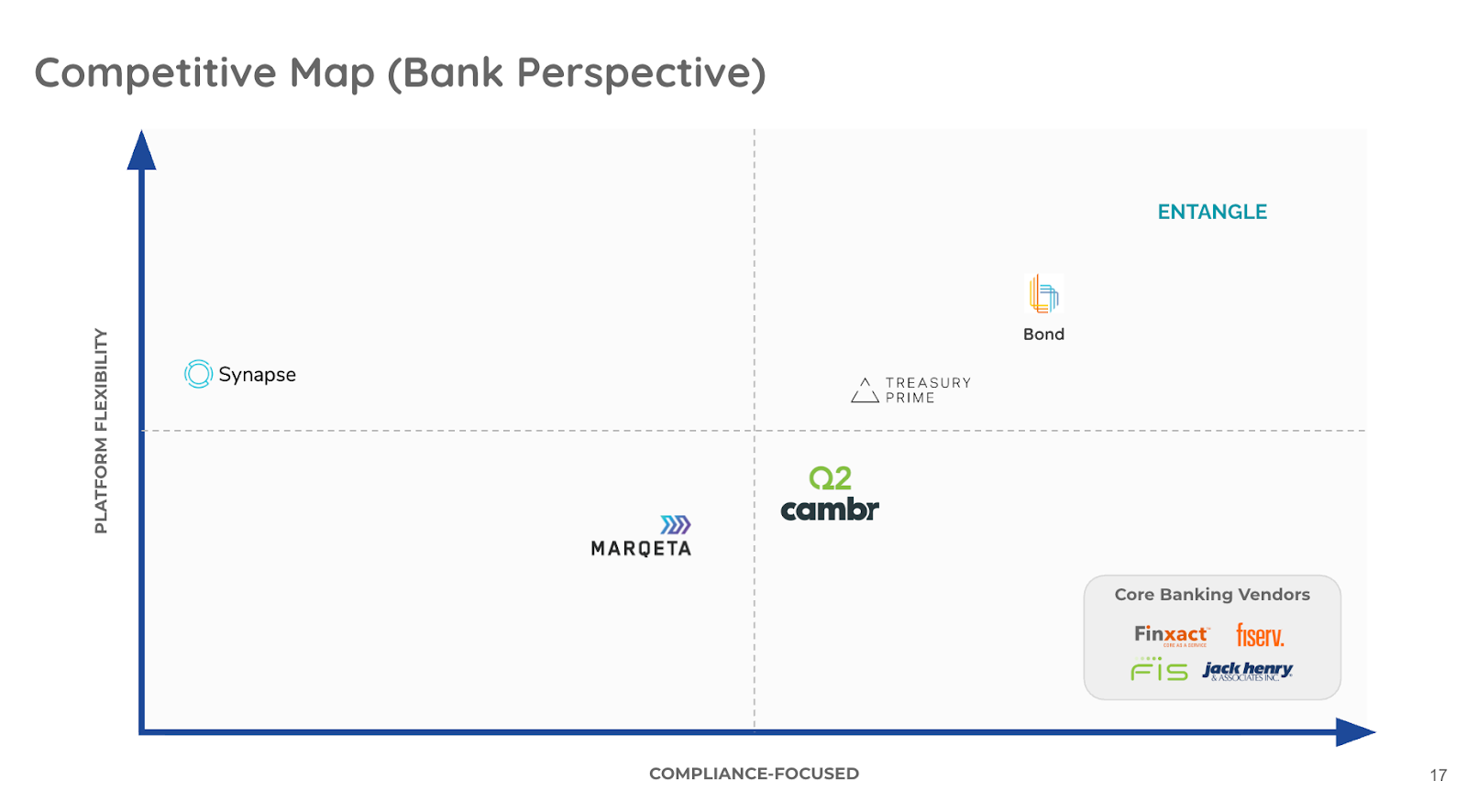

Entangle

How core was risk and compliance to the original machination of Synctera? Well as part of our original pitch deck, we had a chart about where we could fit in. And by we, I mean “Entangle” which was Synctera’s original name:

Back in April 2020, there were platforms that were flexible, but they weren’t necessarily focused on compliance. We would be strong in both, because even then we believed that’s what it would take to 1. Do things right, and 2. Win.

You might recognize the name of the company that fits into the riskier (aka limited compliance) bucket and we all know how that turned out. Sadly for the industry at large, the last few years have been much more challenging than they should have been, because many folks came into the space without any care or thought for compliance and basic banking reconciliation. “Where’s the money” seemed optional in light of growth, and it has taken quite a lot of energy to reset things.

Banks Aren’t Taxis

In the tech world, “slow and steady wins the race” isn’t the mantra that you often hear. It’s more like “move fast and break things” and the latter is the path that we decidedly avoided, because that just doesn’t work in finance and banking.

The market often confuses speed for strength and thinks that everything should be free. At Synctera, we stayed focused and built a moat of resilient growth, with risk and compliance at the core.

You might imagine that building a two-sided marketplace like Uber (banks on one side, FinTechs on the other) would be quite challenging in banking. It was, and that's our moat. What I learned from my time at Uber is that building intentionally for regulatory compliance is a heavy lift, but an amazing asset when done well. Banking regulation exists for real reasons: accountability, trust, and protecting other people's money.

When we went out to raise our seed round, our product deep dive slides didn’t start with “Speed”. Each one started with “Protect.”

We made sure that Synctera was a place that talented people who wanted to modernize banking could safely tinker. That led to really steady growth and a refinement of who we could serve best and with what tools.

Avoiding the storm, deliberately

If we’ve spent any time together, you’ve probably heard me say that “banking is hard” and I find it to be a good reminder. Probably more apropos is that “in banking, things break and weird transactional situations happen all the time”. Experience matters, resilience matters, trust matters. But the core anchor is that it's real people's money we're managing. We have to do and be better.

While banking could, of course, be 'better systemically,' the interconnected nature of the business with thousands of partners makes macro change very difficult. There are various ideas from stablecoins to AI that should improve some of the infrastructure, tracking the dollars and cents, but much of our work is connecting the new to the legacy. Friction abounds. Fundamentally, if you hear “we can launch you in 48hrs,” someone is cutting corners, and risk is being created.

Our six-year journey has been a very deliberate march to stay true to our early core thesis. We’ve built robust compliance infrastructure, lasting relationships with banks, and made breakthroughs on how to do important things like reconciliation at scale. Did we lose deals over the years because of that focus? Sure. We got beaten out by cheap and free quite a few times. Some came back; others shut their programs down after bad experiences elsewhere.

You know what's better than losing the deal? The boomerangs: customers that come back and work with us on their v2. We aren't in the “I told you so” business. We're in the “'let's just build something useful and good” business. We're happy to re-engage with folks that tried something else, and have done so many times. Again, the focus is on the end user and looking after their interests. Ultimately, that's our goal.

Some may think of funding and raising big rounds as a moat, but the real moat that we’ve built at Synctera is the thousands of decisions made always with the intention of doing things safely and sensibly.

Still Building

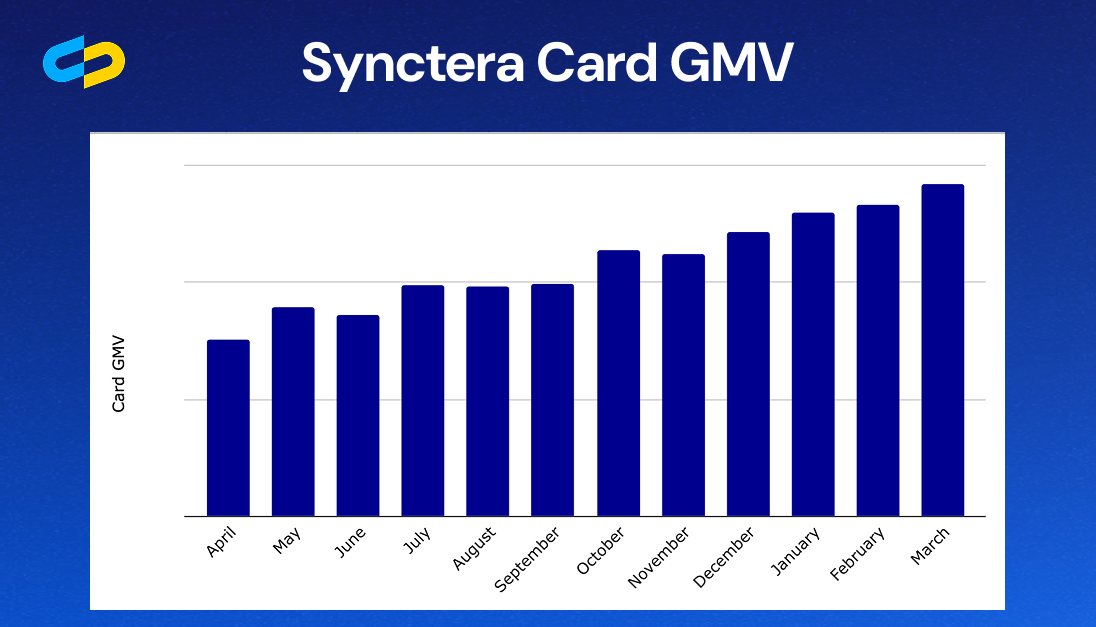

As we start our sixth year, we’re accelerating. These last two months have been our best yet. We’ve signed eight new FinTechs. Synctera-powered card spend is nearly doubling year-over-year, with a multiplier to kick in once credit card programs launch in the next few months. Our bank relationships are growing with four new partners coming online to support our customer launches. We’re also deepening our relationship with our existing sponsor bank partners, adding more compliance features for day-to-day management on top of our flexible core banking system optimized for embedded finance operations.

Our company profile has been quite strong for the last year or so, as we have been able to double our revenue while keeping headcount flat. Technology, and yes, AI, is helping us scale and grow with improved margins . Our platform is expanding and our customers are bigger and more complex every day, embedding ourselves into their success.

While I love working with founders and very early stage startups (I think I spend 5-10 hours a week with them), we are moving up the food chain and are now competing with the biggest, and most established players in FinTech. We have fabulous investors that have helped us on the journey and we’re putting the $100M we’ve raised to date to good use.

I’m so grateful to have such a great management team to help run the business, and just hired our first general counsel, Conway Ekpo. We’re just getting started though, and with break-even in our sights by Q3 of this year, we get to look at what’s next.

The next chapter is about what happens when AI agents are integrated into daily operations. Every meaningful AI workflow eventually hits banking infrastructure, and most of it isn't ready. We're building the orchestration layer that connects AI agents to banking systems the right way: compliantly, reliably, and at scale.

If you want to compete with what we've built over the last 2,200 days or so, there’s a lot to do. If you think “it’s just a ledger, how hard can that be”, please give me a call and I’ll try to help you get there much faster with our platform.

In hindsight, we should have added a slide in that original deck that said “Not speed. Not market size. Endurance.”

The next six years start now.

Great banking products get built and scaled on Synctera’s end-to-end platform

.svg)