Debit, Charge, or Credit: Which Card Program is Right for Your Business?

February 18, 2026

.png)

Launching an embedded card program puts your brand in your customer's wallet (or digital wallet) and unlocks new revenue streams through interchange. However, with card options ranging from standard debit cards to more complex revolving credit lines, choosing the right card "rail" requires careful consideration.

At Synctera, we provide end-to-end infrastructure for companies to launch a card program, providing all of the tech needed to launch: Debit Cards, Charge Cards and Credit Cards.

While the underlying issuing and processing infrastructure is similar regardless of card type, each one comes with its own unique components, operational considerations, and end-user benefits. This guide breaks down each option, explains the trade-offs, and helps you decide which card is the right fit for your embedded card product.

1. Debit Cards

The reliable foundation for everyday spending.

The Synctera Debit Card gives users fast and convenient access to spend the funds they have deposited into their account. Users are only able to spend the balance available in their account, so there is no lending or repayment component.

Each time a user swipes their debit card, the balance of their deposit account is checked against the transaction amount to ensure they have the funds available. If the transaction amount is higher than the available account balance then the transaction is declined. The use of existing funds minimizes the risk of the company issuing the card.

With debit cards being operationally less complex than the other card options, they are often the card type selected by smaller startups or those wanting to launch a card program within a short timeframe. However, compared to the other card options, debit cards have the lowest interchange income limiting the revenue potential for companies offering debit cards.

Benefits for Companies Offering Embedded Cards

- Speed to Market: It allows you to issue cards quickly without the need to account for credit decisioning or underwriting.

- Operational Simplicity: Compared to other card type options, debit cards have the fewest operational workflows and considerations.

Benefits for Users

- Convenient Spending: Users can easily spend at most merchants, both at physical and online locations.

- No Credit Check Required: Unlike credit cards, which users can be denied from accessing.

- Cash Management: Since debit card spending is tied to the account balance, it helps prevent users from overspending.

Best Use Cases

- Introductory Cards: For kids or those new to the financial ecosystem, debit cards provide a way for them to begin spending using a card, without the credit risk.

- Financial Wellness Apps: Helping users stay on budget by only allowing them to spend available funds.

- Immediate Access to Funds Earned: Offering a debit card that is tied to a deposit account provided end-users with a way to immediately spend the funds that are deposited into their account.

2. Charge Cards

The revenue of credit, with the safety of debit.

Charge cards are a unique hybrid. Charge cards run on credit rails to maximize interchange for the issuer, but do not incorporate a lending component like a traditional credit card would. This makes charge cards an ideal choice for companies that want their card program to drive significant revenue, but do not want to manage the workflows involved in offering a true lending product.

Synctera enables companies to offer two different types of charge cards:

- Secured Smart Charge Card: Spending limit is tied to the available balance in the attached deposit account, providing users with credit access while minimizing credit risk for both the user and the issuer. Unlike traditional secured charge card products, Synctera’s Smart Charge Card allows end-users to deposit funds into a full-featured bank account, enabling them to use the account for all of their banking needs.

- Unsecured Charge Card: Spending limit equals a pre-determined credit limit, providing users with additional short-term liquidity, but raises the credit risk of the program. The unsecured charge card does not have a deposit account linked to it, so end-users can only transact using their charge card.

In both cases, no underwriting or credit check is required, making this a great product option for users that are new to credit or looking to rebuild their credit. Additionally, users must pay the balance in full every month and can not carry over an outstanding balance. This aspect of a charge card protects users from overspending, while also reducing potential losses for the issuer of the program.

Benefits for Companies Offering Embedded Cards

- Significant Interchange Revenue: Because it runs on credit rails, you earn credit interchange fees, which can be as high as double the interchange earned from debit cards.

- Limited Credit Risk: User spending is tied to a credit limit or available balance, minimizing the credit risk of the program.

- Speed to Market: No underwriting or lending components are needed to launch a secured charge card.

Benefits for Users

- Credit Building: It provides a structured pathway to demonstrate responsible behavior, helping consumers build or rebuild credit profiles.

- Wider Acceptance: Credit cards generally have higher merchant acceptance rates than debit cards, especially for travel and rentals.

- Consumer Protection: Cards that run over credit rails provide additional consumer protections against unauthorized charges or fraud

- No Interest Payments: Since the balance is paid in full monthly, users pay no interest.

Best Use Cases

- Credit Builders: For immigrants, young consumers, or unbanked users new to the formal credit system.

- Credit Re-builders: For consumers with bad credit profiles or prior defaults who need a safe way to re-enter the system.

- High-Net-Worth Savers: For "super prime" users who want the acceptance and fraud protection of a credit card but prefer to spend within their means.

3. Credit Cards

True revolving credit for maximum differentiation.

The Synctera Credit Card enables companies to launch a true revolving credit card to both businesses and consumers. This allows users to spend against a credit limit and, if necessary, carry a balance (revolve) from month to month with interest.

Credit card usage continues to grow in the US, with the payment method now accounting for the largest share of consumer payments. This makes credit cards the ideal card choice for customers that want to become the go-to spending method for their customer base.

To stand out amongst other card options in the market, companies can tailor their credit card program to the specific needs of their user base, including unique underwriting criteria, rewards, or transaction-level APR groupings.

Benefits for Companies Offering Embedded Cards

- Maximum Revenue: In addition to earning high interchange fees, you can generate significant revenue from interest income (APR) and annual fees.

- Top-of-Wallet Status: Credit cards currently dominate the U.S. market (over 80% ownership for adults), driving significantly higher transaction volumes than debit.

- Differentiation: Offering a bespoke credit card allows you to stand out against competitors by allowing for flexible spend and unique rewards.

Benefits for Users

- Spending Flexibility: Users can spend ahead on a line of credit rather than being limited to stored funds.

- Rich Rewards: The economics of credit cards generally support richer reward programs tailored to the user's needs.

- Credit Building: Users can use the credit card to build their credit history.

Best Use Cases

- Top-of-Wallet Financial Apps: Credit cards are the primary spend method for most Americans, making it a key component of companies that want to be their customers’ primary bank account.

- Corporate Cards: Providing a corporate spend card that is tailored to the businesses unique needs.

- Non-bank Lenders: For companies that offer loans to businesses or consumers, build deeper relationships and increase LTV of those customers by adding a credit card product.

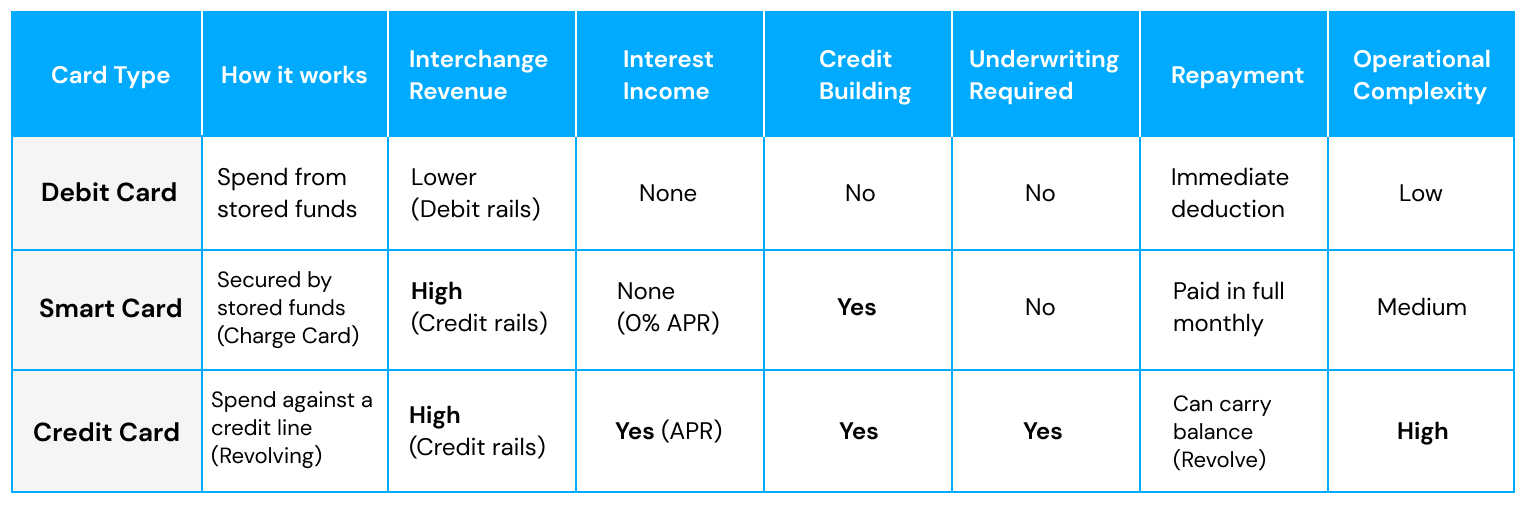

Card Comparison at a Glance

How Synctera Streamlines Your Card Launch

Building a card program on your own is complex, often taking 12–15 months, and costing millions to assemble the necessary components. You have to juggle bank relationships, processor integrations, compliance workflows, and card fulfillment vendors.

Synctera removes this friction with an all-in-one solution that provides the tech and sponsor bank connection you need to launch quickly. Here is how we make it easy:

1. A Single, Unified Platform

Instead of stitching together disparate vendors, the Synctera APIs provide easy integration into all tech components necessary to launch a card program, from customer onboarding and account opening to money movement, card issuing and card management. All customer data lives on a single, unified ledger with a built-in reconciliation engine, improving your operations and compliance.

2. Program Management Support

We don't just give you the code, we have a team of experts that provide support from launch to scale.

- Sponsor Bank Matching: Synctera facilitates conversations with our bank network to match you with the ideal bank for your business.

- Vendor Management: With over 20 ecosystem components integrated into the platform, Synctera handles the vendor relationships and troubleshooting for you.

- Implementation: Synctera provides a detailed project plan and guides you through technical implementation, compliance program development, and operational readiness.

- Operations Support: Synctera’s Ground Control and Payment Ops teams act as an extension of your business, providing support for key workflows like payment investigations, disputes, fraud alerts, and KYC reviews.

3. Powerful Operational Tools

Manage your entire program through the Synctera Console, a complete user interface for your back-office teams. From the Console, you can:

- Manage the full card lifecycle (issuing/reissuing, freezing, and terminating cards).

- Communicate and collaborate on key workflows with the program’s sponsor bank partner.

- View and search for all customer, card, and transaction data.

- Handle operational cases for KYC/KYB reviews, fraud alerts, and disputes.

- View reporting on program growth, interchange breakdowns, or any other aspect of the program.

If you’re evaluating which type of card program is right for your business, reach out to us to talk to one of our experts who can guide you through the process.

Product

Great banking products get built and scaled on Synctera’s end-to-end platform

.svg)